Apply for financing online using our simple application.

We’ll match you with a local dealership who will show you vehicle options you are pre-approved for.

Pick the car you want and drive away! No more wasted time. No more rejection.

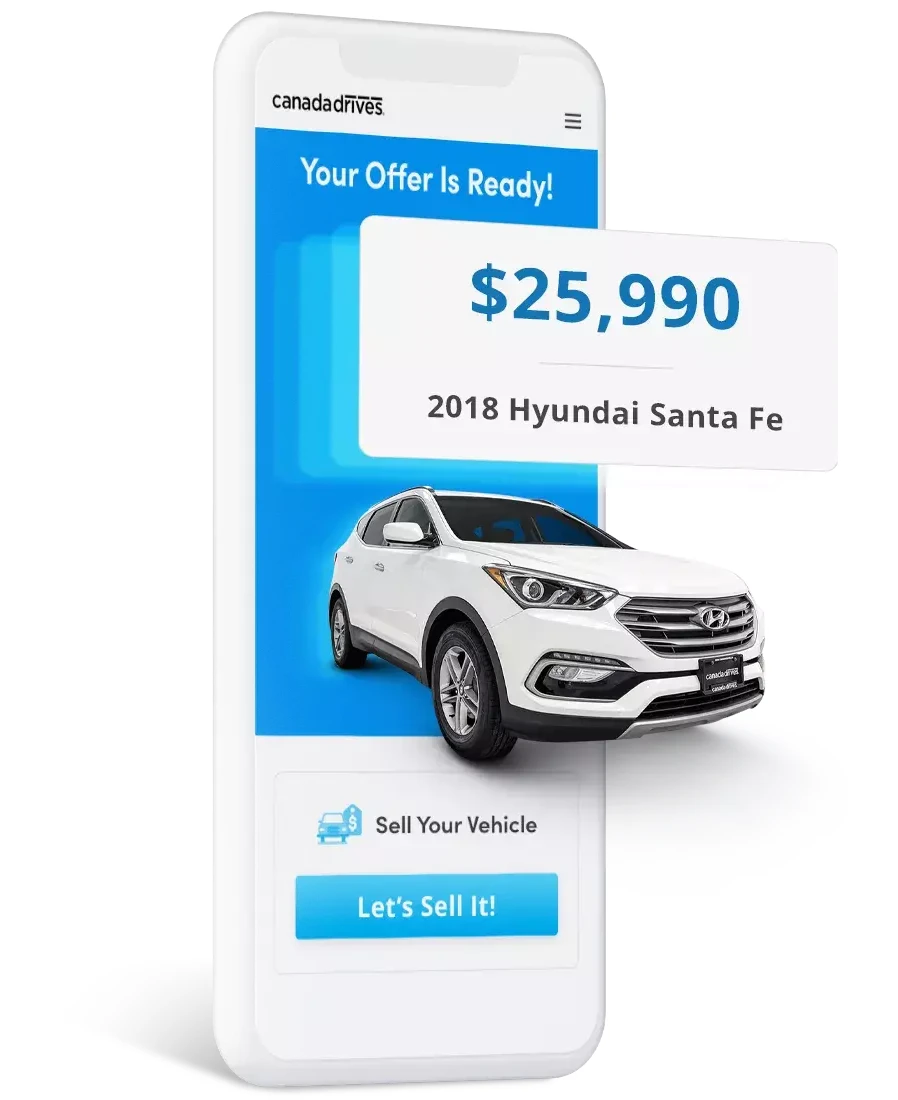

Skip the hassle of selling your car privately and sell your car to us for cash.

Get an instant offer online that is valid for 7 days.

No lowball offers, no wasted time, no meeting strangers.

MelanieNorth York, Ontario

KennethAlliston, Ontario

KeithKelowna, British Columbia