Apr 23, 2026

How to Get a Car Loan After Bankruptcy in Canada

Filing for bankruptcy doesn't have to mean the end of your financial life — or your ability to get reliable transportation. Here's how to get a car loan after bankruptcy in Canada, and what to realistically expect.

TL;DR

You can get a car loan after bankruptcy in Canada — often sooner than you think. Most lenders that work with bad credit situations can help you get financed once your bankruptcy is discharged, sometimes within days. You'll pay higher interest rates and likely need a down payment, but a car loan can also be one of the fastest ways to rebuild credit after a financial fresh start. Specialty lenders and certain dealerships are your best bet, not traditional banks.

Key Takeaways

- You don't have to wait years after bankruptcy to get a car loan — financing is possible shortly after discharge.

- Traditional banks and most major financial institutions are unlikely to approve you right away; specialist lenders are the way to go.

- Expect higher interest rates due to your credit history, but rates can improve after 6–12 months of on-time payments.

- A down payment — even a modest one — improves your approval odds and can get you better terms.

- Making regular car loan payments is one of the most effective ways to rebuild credit after bankruptcy.

- Check both Equifax and TransUnion credit bureaus for errors before applying — mistakes are common after bankruptcy and can hurt your chances.

- Canada Drives connects Canadians in all credit situations (including post-bankruptcy) with dealerships that can actually help.

In This Article

- Managing Your Expectations

- How Long After Bankruptcy Can You Get a Car Loan?

- Finding the Right Lender After Bankruptcy

- Car Dealerships That Accept Bankruptcies

- Getting Financed for a Car After Bankruptcy

- Getting Your Credit Report and Credit Score

- Refinancing Your Car Loan

- FAQ

- People Also Ask

- Related Prompts

- About Canada Drives

It's a common misconception that filing for bankruptcy means you are financially ruined and won't be able to rebuild your credit or obtain a car loan in the foreseeable future. This idea is far from the truth.

According to the Government of Canada, 1 in 6 Canadians will file for personal bankruptcy or file a consumer proposal at least once, so it's a lot more common than you think. If you feel a little embarrassed or afraid of how this will affect your relationships with lenders in the future or whether you'll ever qualify for a car loan, you don't have to be. There are reputable lenders out there that can help you get approved for an auto loan. In fact, Canada Drives has dedicated programs for Canadians facing bankruptcy and other credit problems.

Filing for bankruptcy means wiping out most of your debts — giving your finances a clean slate — and the bankruptcy will stay on your credit record for up to six years. Despite this, it is possible to obtain a car loan at a reasonable interest rate.

Definition: Bankruptcy — A legal process in Canada that allows individuals in serious financial difficulty to eliminate most unsecured debts (like credit card balances and personal loans) in exchange for surrendering non-exempt assets. Once discharged, you get a financial fresh start but carry the bankruptcy notation on your credit report for 6–7 years.

Managing Your Expectations

While it's less likely that you'll be approved for an expensive new car, there are still some good options available out there for people who have gone through bankruptcy.

It's important to be realistic and understand that by filing for bankruptcy, you won't qualify for the same loan terms as you would have otherwise. Be aware of the terms of your loan, which will be different compared to a person with better credit history. As you are considered high risk after a bankruptcy, your interest rate will also be higher.

That said, the goal at this stage isn't the best possible deal — it's getting into a realistic vehicle that fits your budget and monthly income, while starting to demonstrate financial responsibility again. Think reliable transportation, not a brand new truck.

It's also important to keep in mind that the process of buying a car may take a little extra time because lenders will require some information from your trustee. However, if you work with the right company — like Canada Drives — the process should be pretty painless.

How Long After Bankruptcy Can You Get a Car Loan?

This is one of the most common questions Canadians ask after going through bankruptcy — and the answer is better than most people expect.

Technically, there is no legal waiting period to apply for a car loan after you've been discharged from bankruptcy. You can apply the day after discharge. That said, most lenders will look at your current financial situation, your employment status, monthly income, and credit history before making a decision.

Here's a rough breakdown of what to expect at each stage:

- While still in bankruptcy (active): Most lenders won't approve a new car loan while your bankruptcy is still active. It's best to wait until you've been fully discharged.

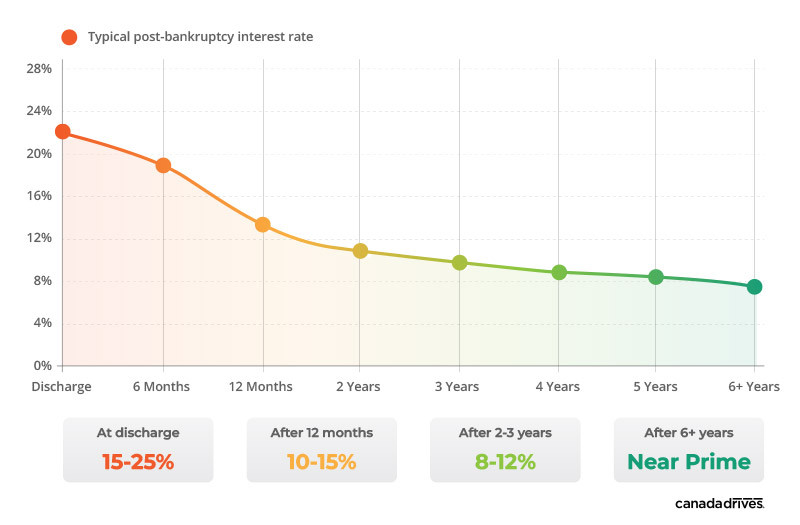

- Right after discharge: Specialist lenders and certain dealerships can work with you right away. Expect higher interest rates (typically 15–25% from subprime lenders) and a requirement for a down payment.

- 6–12 months post-discharge: If you've been making on-time payments on any new credit (including a car loan), you may already start to see your score improve. Some lenders become more flexible in this window.

- 1–2 years post-discharge: More lenders become available to you and interest rates may start to come down, especially if you've maintained clean payment history.

- After the bankruptcy is removed from your credit report (6–7 years): You'll have access to a much wider range of financial institutions and better interest rates.

The short version: you don't have to wait years. But the sooner after bankruptcy you apply, the higher the cost of borrowing will be. If your unique situation allows, even saving a modest cash down payment before applying can make a meaningful difference.

Rates are illustrative ranges based on typical subprime lending in Canada. Individual results vary based on income, down payment, and credit activity since discharge.

Finding the Right Lender After Bankruptcy

If you have just recently gone through bankruptcy or consumer proposal, you won't have to wait years to get financing for a vehicle. In fact, obtaining a car loan and maintaining your monthly payments can help you with rebuilding your credit. At this point, the most important thing is to avoid other bad debts or negative payment history.

The last thing you want to do is invest time hopping from dealership to dealership being turned down or going to a bank only to hear "no." This is not only frustrating but can also adversely impact your credit score — every hard inquiry from a lender gets recorded by the credit bureaus.

Getting approved for a car loan after bankruptcy is a lot easier than it used to be. With our massive network of dealerships, Canada Drives can help any Canadian find the right car, regardless of their credit situation.

Simply provide a few quick personal details via our online form and we will connect you with a local dealership in your area who will show you vehicle options you qualify for.

Definition: Subprime Lender — A financial institution or lender that specializes in offering loans to borrowers with poor or limited credit history. They take on higher risk than traditional banks and typically charge higher interest rates to offset that risk. Post-bankruptcy borrowers usually need to work with subprime lenders before they can qualify with mainstream financial institutions.

Car Dealerships That Accept Bankruptcies

Not every dealership is set up to work with post-bankruptcy applicants — but more are than you might think. The key is knowing where to look.

Traditional franchise dealerships (think big-brand new car dealers) often have strict lending criteria tied to prime or near-prime lenders. They may turn you away or only offer limited options if you've recently been discharged from bankruptcy.

Here's what to look for instead:

- Dealerships with in-house financing: Some used car lots offer their own financing, bypassing banks entirely. They have more flexibility on approval, though terms vary widely — read everything carefully.

- Dealerships connected to subprime lending networks: These dealers have established relationships with lenders who specialize in bad credit and post-bankruptcy situations. They're used to the process and won't waste your time.

- Dealerships that work through platforms like Canada Drives: Canada Drives pre-screens applicants and connects them with dealers who already know your situation before you walk in. This avoids unnecessary paperwork, reduces the number of hard credit inquiries, and means the dealer has real options ready for you.

The advantage of going through a network like Canada Drives is that dealerships in the network are already set up to work with a wide range of credit situations. You're not a potential client visiting cold — they know what you're approved for before you arrive.

When you do visit a dealership, focus on a realistic vehicle within your budget. It's tempting to stretch, but a manageable monthly payment you can consistently afford is far more valuable right now than a newer model. Consistent, on-time payments are what rebuild credit and eventually qualify you for better terms.

Getting Financed for a Car After Bankruptcy

The approval process for a car loan after bankruptcy is a bit different from a standard application. Here's what most lenders will look at:

- Employment status and monthly income: Lenders want to see stable income. A steady job goes a long way — it shows you have the means to make payments. Self-employment income is acceptable but may require additional documentation.

- Down payment: A down payment reduces the lender's risk and increases your approval odds. Even putting $500–$1,000 down can help. A larger down payment (10–20%) can also get you a better interest rate. If you're short on cash, trading in a current vehicle is one way to free up money toward a down payment.

- Discharge status: Most lenders require that your bankruptcy be fully discharged. If it's still active, the approval process is much harder — nearly impossible with most lenders.

- Trustee documentation: Because your credit file shows a bankruptcy, lenders may request information from your Licensed Insolvency Trustee (LIT). This is normal and not something to be alarmed about.

- Credit report: Lenders will pull your credit report from one or both credit bureaus (Equifax and TransUnion). They'll look at your overall credit history, any new credit accounts opened since discharge, and payment behavior.

- Assets: While not always required, disclosing current assets (savings, property) can support your application and demonstrate that you've started to stabilize financially.

One practical tip: try to do all your car loan shopping within a short window (ideally the same week). Multiple hard inquiries from auto lenders within a short period are often treated as a single inquiry by the credit bureaus — this limits the damage to your score during the approval process.

Also, getting pre-approved before you visit a dealership is a smart move. Walking in with pre-approval in hand puts you in a stronger negotiating position and saves time.

Getting Your Credit Report and Credit Score

Although it may be daunting to get your credit information, it's a good idea to get an understanding of where you're at after bankruptcy. After all, the lender will be checking your credit, so you'll want to see what they are looking at and ensure there are no mistakes — which can happen.

You can obtain a free credit report and score online. Your credit report includes information about previous auto loans, so pay attention to those details. The credit-scoring models used by auto lenders are heavily weighted toward credit score, meaning positive on-time monthly car loan payments will work in your favour when re-establishing your credit.

Check both major credit bureaus — Equifax and TransUnion. Errors on credit reports are more common than people realize, and a mistake could make your situation look worse than it actually is. If you find an error, dispute it directly with the bureau. Correcting even one inaccuracy can improve your score meaningfully.

Some things worth checking on your report after bankruptcy:

- Confirm the bankruptcy discharge date is recorded correctly

- Make sure debts that were included in the bankruptcy aren't still showing as outstanding to individual creditors

- Look for any accounts you don't recognize (potential identity theft)

- Check that any new credit accounts opened since discharge are being reported accurately

Definition: Credit Bureau — An organization (in Canada, primarily Equifax and TransUnion) that collects and maintains credit information on individuals. Lenders report borrowing and payment activity to these bureaus, which compile it into a credit report and calculate a credit score. After a bankruptcy, both bureaus will note the filing on your report for up to 6–7 years.

Refinancing Your Car Loan

Don't forget — you will have the chance to refinance your car loan at a later date.

You'll want to keep an eye on your credit score, as you may be able to refinance your car loan at a lower interest rate in the future. If you continuously make on-time payments to your car loan, you will see your score improve after 6 to 12 months.

Refinancing can also be a useful tool for building financial stability. If you started with a high-rate loan right after discharge and your score has improved, refinancing to a lower rate reduces your monthly payment — freeing up money and improving your overall budget. It's not guaranteed, but it's worth checking regularly as your credit recovers.

For more on managing your finances after a rough patch, see our guide on how to get approved for a car loan with bad credit.

FAQ: Car Loans After Bankruptcy in Canada

Can I get a car loan while still in bankruptcy?

In most cases, no. Most lenders — including subprime ones — require that your bankruptcy be fully discharged before approving a new loan. While you're still in the process, focus on working with your trustee, keeping expenses minimal, and preparing for life after discharge.

Will a car loan help me rebuild credit after bankruptcy?

Yes — it's one of the most effective ways to do it. Both Equifax and TransUnion record your payment history on installment loans like car loans. Consistent, on-time monthly payments will gradually improve your credit score. Many people see meaningful improvement within 6–12 months.

How much of a down payment do I need after bankruptcy?

There's no fixed minimum, but most lenders prefer to see at least 10–20% down for post-bankruptcy applicants. Even a smaller down payment helps. The more cash you can put down, the lower the lender's risk — which typically means better terms and a higher chance of approval.

Will banks give me a car loan after bankruptcy?

Traditional banks and credit unions are unlikely to approve you shortly after discharge. Most mainstream financial institutions want to see at least 1–2 years of rebuilt credit before they'll consider a post-bankruptcy applicant. Your best options in the near term are subprime lenders and dealerships that specialize in bad credit financing.

Does applying for a car loan hurt my credit score?

Yes, each hard credit inquiry can slightly lower your score. That's why it's smart to get pre-approved through a service like Canada Drives rather than applying at multiple dealerships. Also, multiple auto loan inquiries made within a short window (typically 14–45 days) are often counted as a single inquiry by the credit bureaus.

What interest rate can I expect on a car loan after bankruptcy?

Expect rates between 15–25% from subprime lenders right after discharge. Rates vary based on your income, down payment, time since discharge, and any new credit you've established. As your credit improves, you may be able to refinance to a lower rate.

Can I get a car loan after a consumer proposal?

Yes. Consumer proposals are treated similarly to bankruptcy by most lenders. The same general rules apply — you'll need to be discharged, show stable income, and likely work with a subprime lender initially. Canada Drives works with applicants who have been through consumer proposals as well.

People Also Ask

How long does bankruptcy stay on your credit report in Canada?

A first-time bankruptcy stays on your credit report for 6 years from the date of discharge (or 7 years in some provinces). A second bankruptcy stays for 14 years. Even though it remains on your report, you can start accessing new credit — including car loans — well before it's removed.

What happens to my car when I file for bankruptcy?

It depends on whether your car loan is secured or unsecured. If the car is collateral on a loan (secured debt), the lender may have rights to it. If you're current on payments and wish to keep the car, you may be able to continue making payments and keep it. Your Licensed Insolvency Trustee will review your specific situation. If you owe significantly more than the car's market value, surrendering it and including the shortfall in the bankruptcy may make more financial sense.

What do lenders look for when approving a car loan after bankruptcy?

Lenders look at your employment status, monthly income, time since discharge, down payment amount, any new credit activity, and documentation from your trustee. Stable income is often the most important factor — it shows you can afford the payments going forward.

Is it better to buy new or used after bankruptcy?

Used is almost always the better choice right after bankruptcy. New car loans typically come with stricter lending criteria and higher purchase prices. A reliable used vehicle with a lower price point means a smaller loan, lower monthly payments, and a more manageable budget — all of which support financial recovery.

Does a consumer proposal affect my ability to get a car loan?

Yes, but less severely than a full bankruptcy in some cases. Both appear on your credit report and signal financial difficulty to lenders. Most people who have completed a consumer proposal can access car financing through subprime lenders fairly quickly after their proposal is discharged.

Related Prompts

- "How do I get approved for a car loan after bankruptcy in Canada?"

- "Which car dealerships in Canada accept bankruptcies?"

- "How long after bankruptcy can you finance a car in Canada?"

- "How does a car loan help rebuild credit after bankruptcy?"

- "What down payment do I need for a car loan with bad credit in Canada?"

About Canada Drives

Canada Drives helps Canadians get pre-approved for vehicle financing before they start shopping. Our online application matches drivers with local dealerships that have vehicle options for all credit situations, including bad credit or limited credit.

With one simple pre-approval, you can avoid wasted time at the dealership and shop with confidence knowing exactly what you're approved for.