Feb 25, 2026

How to Get Approved for a Car Loan with Bad Credit in Canada

Struggling to get a car loan with bad credit in Canada? You’re not alone — and you’re not out of options. Even if banks have said no, there are still lenders, dealerships, and online retailers that specialize in helping Canadians get approved and rebuild their credit at the same time.

TL;DR

You can get approved for a car loan in Canada with bad credit, even without a cosigner. Specialized lenders focus on income, employment stability, and down payment instead of just your credit score. Getting pre-approved, choosing a used vehicle, and making on-time payments can help you rebuild your credit while driving a reliable car.

Key Takeaways

- Credit scores below 660 can make traditional bank approvals difficult.

- A steady monthly income (around $1,800 before taxes) significantly improves approval chances.

- Used vehicles increase approval odds and reduce monthly payments.

- A down payment or cosigner can help — but isn’t mandatory.

- Specialized dealerships work with subprime lenders to secure approvals.

- On-time car payments improve your credit score over time.

- “Guaranteed approval” usually has conditions — always review the terms.

How to Get Approved for a Car Loan with Bad Credit in Canada

Canadians with bad credit (or no credit) often have a more difficult time getting approved for car loans. But it doesn’t have to be that way! When it comes to bad credit car loans, new opportunities are on the horizon. There are lenders, dealerships, and retailers that specialize in helping bad credit customers find affordable car finance. We reveal how you can get a car loan with bad credit. It might be easier than you think.

Let’s start by stating the obvious: your credit history is important.

Whether you’re seeking a loan, buying a car, or applying for a mortgage, your credit score traditionally decides whether you get approved or declined at crucial moments in your life. But if your credit score is bad now, don’t worry – you can improve it. And in the meantime, you can still get pre-approved for a car loan with bad credit.

You just need to know where to look....

Get pre-approved for your car loan today. Regardless of your credit rating, we know how to get you in the driver’s seat of a vehicle you’ll love and at a price that makes sense! It only takes 3 minutes to get pre-approved online.

Two main reasons why people with bad credit struggle to get approved

1. Your credit score

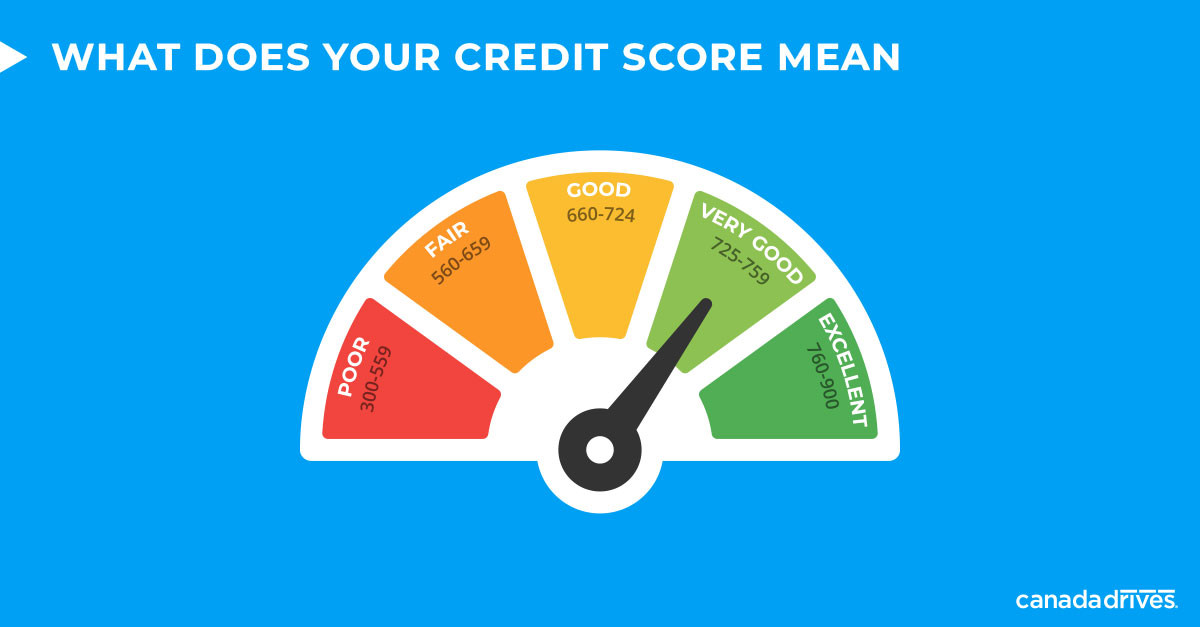

Credit scores in Canada range from 300 points to 900 points. According to Equifax, one of Canada’s major credit bureaus, a good credit score of 660 will likely qualify you for a loan. However, any score of less than 660 might make it challenging to get approved for new credit.

Credit score ranges in Canada.

Considering the average credit score in Canada is on the brink of subprime (a score below 660), applying for credit can be a frustrating process for a lot of people.

Repairing your credit might seem next to impossible when your credit is poor. You see, one of the best ways to rebuild credit is by making regular payments on a loan to show lenders you are reliable. But here's the kicker: you find it difficult to get approved for a loan because you don't have good credit.

Having a great credit score means you can simply waltz into a bank or credit union and get approved for an auto loan without any fuss. However, for a Canadian with low or no credit history, it gets a bit trickier.

When the banks say “no”, there are easier ways to get car finance. There are providers that specialize in helping customers with bad credit, and they can help you get approved for a vehicle that fits your budget and lifestyle. With a bad credit auto loan, a customer not only gets into the driver's seat of a new car but also gets an opportunity to rebuild their credit history.

2. Your income

If you have bad credit, you can still get approved for an auto loan if you go through a dealership or retailer that knows how to help. Some lenders will look at other factors besides your credit score, like your income. Typically, the minimum income for a person to qualify for an auto loan with low credit is $1,800 every month before taxes or deductions (i.e. CPP, EI, etc.).

To put your income requirements into perspective, here’s the breakdown:

Hourly Income:

At least $10.50 per hour for 40 hours per week, or equivalent

Weekly Income:

At least $420 per week (before deductions)

Bi-weekly Income:

At least $845 every two weeks (before deductions)

Twice per month:

At least $900 twice per month (before deductions)

Monthly Income:

At least $1,800 per month (before deductions)

Meeting the minimum income requirements isn’t necessarily make-or-break when it comes to qualifying for car financing. In fact, some lenders will even work with customers who earn their income from government programs. But if you have steady employment, that’s half the battle. A stable job and steady paycheck show lenders that your financial situation is improving, which can dramatically increase your chances of approval.

What Lenders Actually Look At

When most people think about car loan approval, they assume it’s all about their credit score. In reality, lenders evaluate several factors — and your score is just one piece of the puzzle.

Here’s how lenders typically prioritize applications:

Lender approval factors for bad credit car loans in Canada.

How to get a car loan with bad credit

Here are a few tips that could help you secure approval for car finance with poor credit.

What you’ll need:

-

Proof of Employment (recent pay stubs or a letter from your employer)

-

Bank Statements (to show your income deposits and financial stability)

-

A Mobile Phone (so the lender or dealer can easily reach you)

-

A Driver's License (valid ID, ideally with your current address listed)

Having these documents ready will streamline the car loan application process.

Understand your budget

If you want to find vehicle options that fit your budget, you should form an idea of how much you can afford every month. Our car loan calculator will give you a rough estimate of what to expect. If you want to trade in your current vehicle for something newer, your trade-in vehicle will lower your monthly payment, so make sure you factor that in. You can also sell your current car directly to Canada Drives and put the proceeds towards your new car. Get your instant online offer here.

Make sure your expected monthly payment fits comfortably in your budget. While a longer term can result in lower monthly payments, remember that extending the term (the set period of the loan) means you’ll pay more interest over time. It’s all about finding a balance that suits your budget without straining it.

Consider a used vehicle

Look in the used car market. It’s extremely robust in Canada, so whether you want a truck, SUV, or passenger car, you’re bound to find what you’re looking for there. You’ll get almost all the benefits of a new car but at a lower purchase price. Also, depreciation isn’t as big of a concern when you shop pre-owned. A less expensive used car means you’ll need to borrow less money, which increases your approval odds and keeps your payments more affordable. (Leasing a vehicle might appear to be an alternative path if your credit is shaky, but keep in mind car leases also require a credit check and may not be easier to get with bad credit. You’re typically better off buying a reliable used car with a loan you can afford; this way you own the vehicle and can use the loan to rebuild your credit.)

Get pre-approved online

While some dealerships and lenders are not equipped to help bad credit customers, online retailers like Canada Drives can help you get pre-qualified for free and connect you with dozens of great vehicle options. With a pre-approval in your back pocket, you’ll know exactly how much you can afford, saving you a lot of time and frustration. The entire process can often be started from home – you can apply online in minutes and get an answer quickly. Whether you choose a bank or an alternative lender, a pre-approval gives you confidence to start shopping for a car within your price range.

What happens after you apply?

If you’ve never applied for a car loan online, you might wonder what happens behind the scenes. The process is actually straightforward, and much faster than most people expect.

Here’s what the pre-approval journey looks like:

Step-by-step online car loan pre-approval process.

Decide on a down payment

Decide whether or not you want to make a down payment and how much your down payment should be. The down payment is a percentage of the purchase price paid upfront. With a down payment, your chances of approval are even higher, and you’ll have lower monthly payments since you’re financing a smaller amount. Generally, the larger the down payment, the better – a higher down payment reduces the lender’s risk. But a down payment isn’t possible for everyone, and there are also no money down options you can explore. Canada Drives can help you find the option that’s right for you.

Decide on a cosigner

Do you have a cosigner ready to sign, or will you be the only name on your car loan agreement? A cosigner is a trusted friend or family member who agrees to share responsibility for your loan. A cosigner can boost your chances of approval because he/she decreases the level of risk for the lender. Having someone with a higher credit score back your loan can also help you qualify for lower interest rates. However, like a down payment, a cosigner isn’t a viable option for everyone and you can still get approved without one.

Getting a Car Loan with Bad Credit and No Cosigner

What if you have a bad credit score but cannot find a cosigner? Getting a car loan with bad credit and no cosigner is certainly possible. You just need to take a few extra steps to strengthen your application:

-

Review and improve your credit: Check your credit report for any errors or issues that you can fix. Sometimes correcting mistakes or paying off a small outstanding debt can bump your score up slightly. Even a slightly higher credit score improves your odds of approval and might get you a better interest rate. While you might not have time to dramatically boost your score, understanding your credit situation will help you address any red flags in advance.

-

Offer a strong down payment: If you don’t have a cosigner, consider putting more money down. A larger down payment shows the lender you’re serious and willing to invest in the purchase, which makes the loan lower risk for them. As mentioned, even a few hundred dollars can boost your approval chances. Plus, a big down payment means you finance less and enjoy lower monthly payments.

-

Show steady income and employment: Lenders want to know you can afford the loan on your own. Be prepared to provide proof of a stable job and steady income (for example, pay stubs or bank statements showing regular deposits). Meeting that typical minimum income of around $1,800/month (before taxes) is a good benchmark. The more stable your income, the more comfortable a lender will be approving you without a cosigner.

-

Consider a cheaper car or shorter term: Without a cosigner, you may need to start with a less expensive vehicle or a shorter loan term. A smaller loan and shorter term mean less risk for the lender. You can always refinance or upgrade later once you’ve built some payment history and improved your credit.

-

Apply to specialized lenders or brokers: Not all lenders are the same. Many traditional banks may turn you down without a cosigner, but there are car loan providers who cater to bad credit borrowers as solo applicants. These providers will look at your whole financial situation rather than just your credit score. They might approve your loan based on factors like your income, employment length, and down payment, even if you have a low credit score.

By taking these steps, you can greatly improve your chances of getting approved on your own. Remember, every on-time payment you make on your new auto loan will help rebuild your credit, so it’s a win-win situation.

Bad Credit Car Dealerships

When your bank or regular dealership says “no,” it’s time to explore bad credit car dealerships. These are dealerships (and online car retailers) that specialize in helping people with low credit scores get approved for vehicle financing. Unlike most lenders at a bank or credit union who often have strict credit score cutoffs, bad credit car dealerships partner with various subprime car loan providers to arrange financing for customers with less-than-perfect credit.

Bad credit dealerships understand that many Canadians have had credit challenges. They will look at your financial situation more holistically. This means they consider factors like your income, employment stability, and down payment in addition to your credit score. If you have a steady paycheck and can make some down payment, these specialized dealers will work to find a loan that fits your budget. They essentially arrange financing for you through their network of lenders, so you don’t have to go lender to lender on your own. This way, you can secure a car-specific loan instead of trying to use a high-interest personal loan for your car purchase.

Another benefit of working with a bad credit dealership is convenience. You can often apply online or in person and get an approval decision quickly. Then you can choose a car from their lot (or website) knowing financing is already lined up. Many of these dealerships can pre-approve almost anyone, even people with past bankruptcies or very low credit scores, as long as basic requirements are met. They might offer flexible financing options including longer terms or special programs for credit rebuilding.

Importantly, be aware that financing through a bad credit specialist may come with higher interest rates than prime loans. Since they work with subprime lenders, the rates reflect the higher risk. However, if you make your payments on time, you can improve your credit and potentially refinance later for a better rate. In the meantime, you’ll have reliable transportation and a chance to show lenders you can handle an auto loan. The bottom line: if traditional lenders have turned you away, a bad credit car dealership can be your way forward. With their help, you could apply today and be on the road in your new vehicle in no time.

Bad Credit, No Cosigner Car Dealerships

Some dealerships take their bad credit support a step further by advertising themselves as “bad credit, no cosigner” car dealerships. This means that even if you have a low credit score and no cosigner, they are willing to work with you. These dealerships recognize that not everyone has someone with a high credit score available to co-sign their loan, so their programs are designed so that you alone can qualify.

At bad credit, no cosigner car dealerships, the approval will hinge on things like your income, employment, and down payment instead of a cosigner’s credit. You’ll still need to meet basic requirements (stable job, minimum income such as around $1,800 a month, and usually a valid driver’s license plus proof of current address). If you can demonstrate you have the ability to make the car payments on your own, these dealers will find a way to get you approved with only your name on the loan.

Keep in mind that because the lender has no second person to fall back on, they may require a bit more from you as the sole borrower. This could mean a larger down payment or verifying you’ve been at your job for a certain set period (for example, 3+ months of continuous employment) to ensure your income is stable. They may also limit the amount you can borrow until you establish some payment history. It’s all about ensuring you don’t take on more than you can handle.

The good news is that lots of people in Canada get car loans this way. Many Canadians manage to finance a car on their own through these specialized dealerships. Just like any other loan, as long as you make your payments consistently, you’ll not only have a vehicle but also steadily rebuild your credit. And because these dealerships focus on helping people in unique situations, they often have staff who can guide you through the process and answer any questions as you go through your loan application.

Guaranteed Approval Car Loans

While researching bad credit car financing, you might come across ads for “guaranteed approval” car loans. Guaranteed approval sounds great – who wouldn’t want a 100% chance of getting approved? In reality, guaranteed approval car loans are mostly a marketing promise. What it usually means is that certain dealerships or lenders are extremely confident they can get almost anyone approved, one way or another.

Typically, a “guaranteed” approval still comes with conditions. You will need to provide proof of income, have appropriate identification (like your driver’s license and proof of address), and sometimes provide a minimum down payment. Essentially, as long as you meet their basic criteria, they guarantee they will find you some financing option. These dealerships often work with many different lenders or have in-house financing to make good on their guarantee.

It’s important to go into these offers with realistic expectations. A guaranteed approval doesn’t mean you’re guaranteed the best interest rate or any car on the lot. Often, you may be approved for a loan, but at a higher interest rate or with a strict repayment schedule to ensure the lender gets their money back. You might also be limited to certain vehicles that fit a price range deemed affordable for you. For example, they might approve you up to a certain loan amount based on your income and budget.

Before jumping on a guaranteed approval offer, read the fine print. Make sure there are no hidden fees and that you truly can afford the payments on the car they’re offering. Ensure the loan terms align with your budget so you don’t end up struggling with late payments. The upside is that these programs can get you driving when others have turned you down. Just be sure the loan terms are manageable, so that using the loan to rebuild your credit doesn’t put you in a difficult spot. Used responsibly, a guaranteed approval car loan can be a lifeline to rebuild your credit – just remember that “guaranteed” doesn’t always mean the deal is perfect, so it’s wise to compare offers if you have more than one option.

How does a car loan help improve bad credit?

If you don’t know where your finances stand before applying for auto financing, it’s best to do some digging to figure out where your credit score lands. You can download your credit report and learn your credit score for free at Borrowell. If your score is poor or fair, you might want to look at ways to improve it. With a few small adjustments, you could see your credit score increase in as soon as 30 days. Fortunately, a car loan can help you build up your credit score!

But how?

Making your car payments on time every month will help improve your credit rating because your payment history contributes to 35% of your credit score. Good payment history tells lenders you are a reliable borrower who will pay them back. With a better credit score, you'll qualify for better interest rates on future loan products!

FAQ

Can I get a car loan in Canada with bad credit?

Yes. While traditional banks may decline applications below a 660 credit score, specialized lenders and dealerships work with subprime borrowers and consider income and employment stability.

What income do I need to qualify?

Typically, around $1,800 per month before taxes. However, some lenders may consider alternative income sources.

Do I need a cosigner?

No. A cosigner can improve approval chances and rates, but many dealerships offer bad credit, no-cosigner financing options.

Is guaranteed approval really guaranteed?

Not exactly. It usually means approval is likely if you meet basic requirements like proof of income and ID. Terms and rates may vary.

Will a car loan improve my credit?

Yes. On-time payments contribute to 35% of your credit score, helping rebuild your financial profile.

People Also Asked

What credit score is considered bad in Canada?

Generally, scores below 660 are considered subprime and may limit traditional lending options.

Is it better to buy used with bad credit?

Yes. Used vehicles cost less, require smaller loans, and improve approval odds.

How long does it take to rebuild credit with a car loan?

You may see improvements within a few months of consistent on-time payments.

Can I refinance later?

Yes. Once your credit improves, refinancing may help you secure a lower interest rate.

Are online car loan approvals safe?

Reputable lenders and retailers offer secure applications. Always verify the company and review terms carefully.

Related Prompts

- “Create a step-by-step plan to rebuild my credit score in Canada within 12 months.”

- “Compare bad credit car loans vs. personal loans for buying a used car.”

- “How to negotiate interest rates on a subprime auto loan.”

- “Create a monthly budget that includes a car payment and saving

Canada Drives makes car shopping easy!

Canada Drives helps Canadians get pre-approved for vehicle financing before they start shopping. Our online application matches drivers with local dealerships that have vehicle options for all credit situations, including bad credit or limited credit.

With one simple pre-approval, you can avoid wasted time at the dealership and shop with confidence knowing exactly what you're approved for.

More content about